14 SEPTEMBER 2021

Welcome to BLK Shipping, our regular update from the shipping market. In this issue, we’ll be covering:

- Wet Cargo

- Dry Cargo

- Containers

- Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

The increasing price of crude oil has been driving the tankers’ charter rates up throughout July, although this has now slowed down and we are seeing a further downward trend in rates.

VLCC – Very Large Crude Carriers remained pretty much stable. Although we’re still unbelievably far from 2019 levels, we can now see positive signs of pick-up. Outlook: Stable

Suezmax – rates remained still, apart for a few routes where we saw a near 100% growth. As the oil price stabilises, we expect that the vessel charter rates will go with it. Outlook: Stable

Aframax – afra rates more lost ground, with a general weakening across most routes. Outlook: Stable

Dirty Products – Relatively busy in the Mediterranean, whilst supply and demand remaining weak in all other regions. Outlook: Stable.

Clean Products – Charter rates weakened across the board with some routes losing over 70% WoW.. Outlook: Stable

MR – uptake in demand did not have the expected positive effects on MR rates, owing to the oversupply of carrying capacity in the market. Outlook: Stable

LR1 – demand for log-range tankers fell in the last few weeks. Outlook: Stable

LR2 – Good rally for LR2 tankers, up to 20% surge in a week. Outlook: Positive

Handy – Handy earnings bounced back up above $7000/day and it looks like the beginning of a positive performance. Outlook: Stable

Dirty Panamax – Rates continued softening very slightly on all routes, with a general 1% – 5% drop since last week. Outlook: Stable

Dry Cargo

Slow-down on most routes and across all segments, although bulkers remain pretty strong compared to 2019 and 2020 performance.

Capesize – Capes declined between 5 to 20%, having broken through the $40k/day for the first time in years and now travelling on $41k+/day for scrubber-fitted vessels. Outlook: Stable

Panamax – Still another good week for the panamaxes, although slightly in decline compared to the last week of August. Outlook: Stable

Supramax – Supramaxes lost ground in recent days, after climbing steadily over the course of 2021. The second half of August and early September saw a reduction of 4-7% to settle on an average of $35k/day Outlook: Stable

Handysize – the biggest fluctuations happened within the Handy market. Still high after a strong July-August rally, now it fell slightly to $32k+/day mark. Outlook: Stable

Container

Container rates seem unstoppable, with 4400 TEU vessels now nearing the $100k/day mark themselves. Neo-panamax vessels are now close to the $145k/day mark, with a significant impact on the economy of most western countries coming out of the pandemic.

On the raw materials side, however, and especially in chemical commodities, the high freight rates (now looking upwards of $20,000 per TEU on the route China – Europe) now impact prices of goods to the extent that it is equivalent or cheaper to source from European suppliers.

We expect to see a continual decrease in smaller-batches shipments westbound from Asia to Europe, hopefully accompanied by a subsequent easing of the TEU rates towards the end of the year.

Outlook: Positive

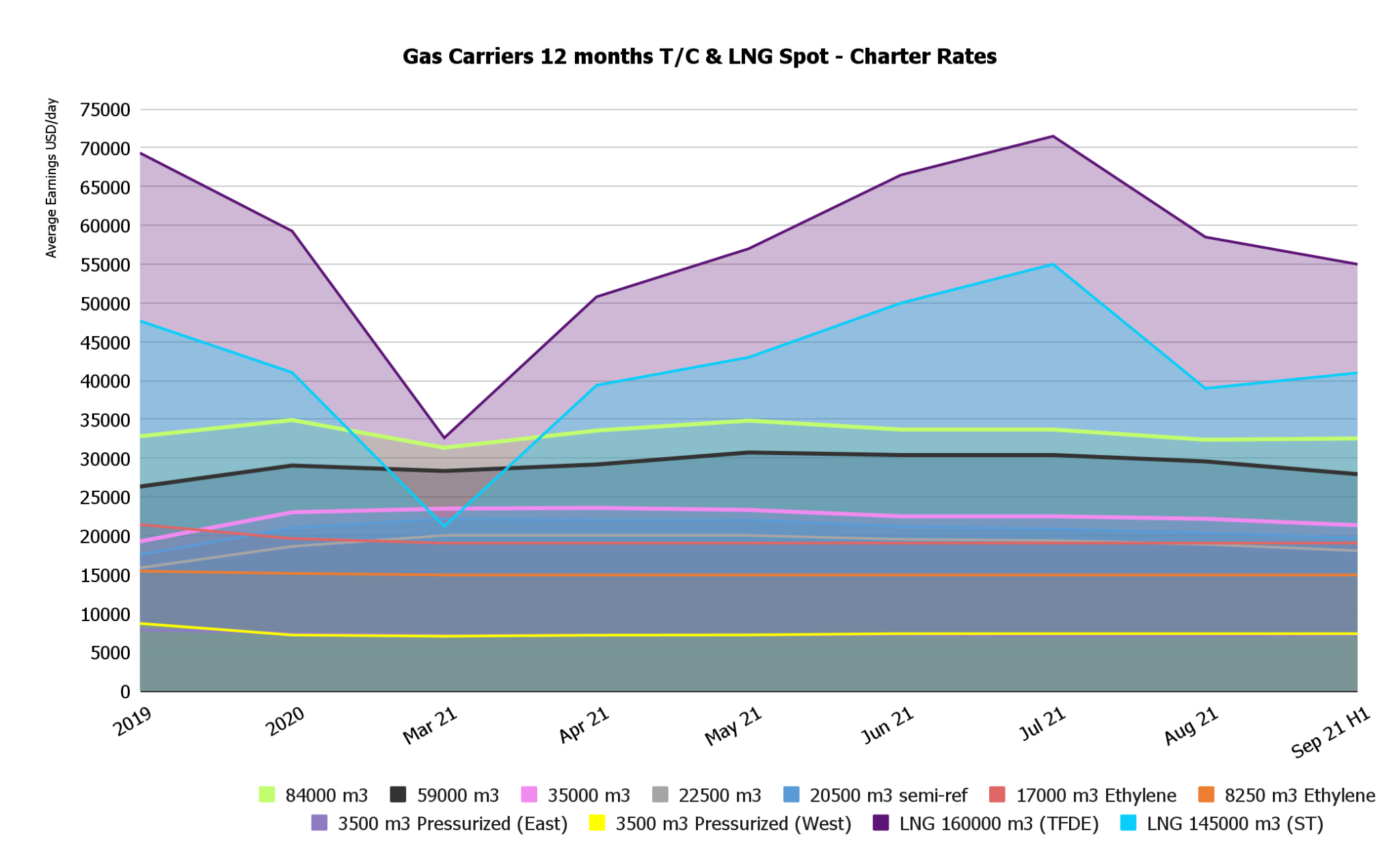

Gas

Rates for Gas Carriers remained declined slightly, with the biggest hit suffered by for large carriers 145,000 m3 and above. Pressurized and semi-pressurized vessel rates remained constant.

This was expected as plenty of tonnage was tied-up in dock for ballast water treatment systems installation and is now slowly coming back into the market, increasing overall supply. Outlook: Stable

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK. Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.