17 OCTOBER 2021

Welcome to BLK Shipping, our regular update from the shipping market. In this issue, we’ll be covering:

- Wet Cargo

- Dry Cargo

- Containers

- Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

The increasing price of crude oil has been driving the tankers’ charter rates up, although the availability of VLCCs meant a general slowdown for this segment.

VLCC – Very Large Crude Carriers saw a decline over the past week, primarily due to the oversupply of tonnage in the market. Outlook: Stable

Suezmax – strong rally Sith over 1800% increase WoW for suezmaxes, with a very strong performance, especially in the Mediterranean. Outlook: Positive

Aframax – afra rates more gained ground, with a general strengthening across most routes. Outlook: Positive

Dirty Products – Apart from the usual busy market in the Med and Black Sea, demand remained weak in all other regions, causing rates to soften. Outlook: Stable.

Clean Products – Charter rates weakened across the board with some routes losing over 50% WoW. The MR market remained relatively oversupplied, and the lack of available cargoes did the rest to cause charter rates to slip by an average of 10% Outlook: Negative

MR – weakening demand did not support the MR rates, which, coupled with the oversupply of carrying capacity in the market, caused rates to fall across the board. Outlook: Negative

LR1 – demand for log-range tankers fell in the last few weeks and continues on a downward trend. Outlook: Negative

LR2 – LR2 tankers weakened approx. 20% WoW but, on average, remain still strong compared to this summer. Outlook: Stable

Handy – Handy earnings weakened too, returning below $3500/day and losing all the ground gained in September Outlook: Stable

Dirty Panamax – Rates softened on most routes, bringing Panamax rates down 22% compared to last month. Outlook: Negative

Dry Cargo

Strong performance for the bulkers on most routes and across all segments, with rates at their highest levels in over 10 years.

Capesize – Capes grew up to 30% in the last week, averaging nearly $73k/day and rates climbing sharply to unchartered heights. Outlook: Positive

Panamax – Still another good week for the panamaxes, although slightly in decline on the Atlantic and on the routes Indonesia to China. Outlook: Positive

Supramax – Supramaxes lost ground in recent days, after climbing steadily over the course of 2021. The second half of September saw relatively steady rates, settling on an average of $30k/day Outlook: Stable

Handysize – Handy market still performing very well. After a strong July-August rally, a slow-down in September now it settled on $36k+/day with short voyages routes fetching over $40k/day. Outlook: Stable

Container

Container rates finally found some market resistance, with Neo-panamaxes vessels finding difficult to push much above the $145k/day mark.

Backlogs in major ports are gravely disrupting supply chains, with queues of over 70 container vessels at Long Beach and other major ports in the US, Europe and China.

We are now seeing, as predicted, a decrease in smaller-batches shipments westbound from Asia to Europe, accompanied by a subsequent easing of the TEU rates which now came down on the high $8000s mark.

Outlook: Stable

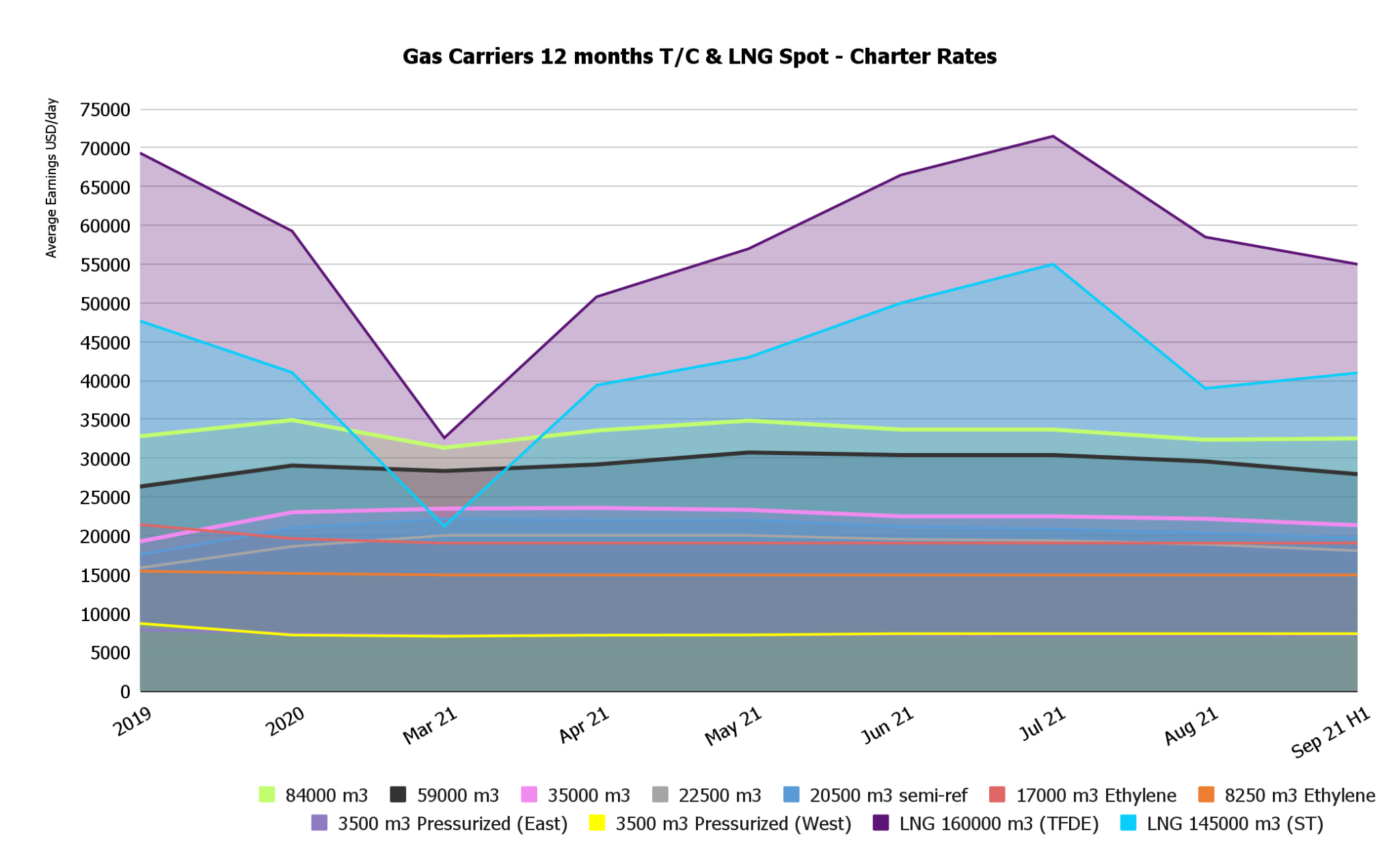

Gas

Rates for Gas Carriers rallied, driven by the strong demand for gas worldwide and the surge in prices across Europe and North America.

Pressurized and semi-pressurized vessel rates remained constant, whilst the biggest winners appeared to be LNG carriers, with rates now nearing the $85k/day for 160000 m3 vessels.

Outlook: Positive

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK.

Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.

Did you miss our previous shipping article? Read it now.