Welcome to BLK Shipping Weekly, our Friday’s update from the shipping market. In this issue, we’ll be covering:

- Wet Cargo

- Dry Cargo

- Containers

- Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

Charter rates down, on all most vessel types, with the rare exceptions of Aframaxeson UKC. Good news for cargo owners, especially for unrefined products, which saw rates slumping by up to up to 61% WoW.

VLCC – It was a bloodbath for VLCCs this week, with some routes commanding negative charter rates. Very good news for shippers, especially those looking at cross-Atlantic routes. List of uncharted vessels remain high, with supply overpowering demand. Owners are now starting to turn down cargoes, in a bid to drive charter rates back up. Avg. VLCCs rate at $1300, significantly below OPEX costs. If you can, ship now. Outlook: Negative

Suezmax – rates still suffering from the oversupply of tonnage in the market. Ships coming out of charters increasing the supply of tonnage and driving rates down. Down on all major routes from 5 to 21% and rates now surpassing those of VLCCs, at $1900 on average. Outlook: Negative

Aframax – afra rates saw drops between 11 and 12%, on some routes, with demand for hold space still counterbalanced by relatively large supply of tonnage. Busier in the Med and Black Sea but not enough to counterbalance the availability of carrying capacity. Avg. charter rates set at $4900/day. Outlook: Stable

Dirty Products – softer rates, primarily driven by the low availability of tonnage in the Mediterraneand and Baltic, with rates down between 3% and 40% WoW Outlook: Stable.

Clean Products – weak to stable rates, owing to the fact that most world refineries are still operating under capacity due to the low demand for refined fuels. With airlines still down and road traffic at a fraction of the pre-pandemic levels the market remains far from its best shape, however, some routes saw near 600% increase which makes the general outlook look better for the weeks to come. Outlook: Positive

MR – uptake in demand drove rates up, with a positive outlook for the weeks ahead. Outlook: Positive

LR1 – demand for log-range tankers remains low. Slow pick-up is possible depending on the easing of lockdowns and demand for refined products on each side of the Atlantic. Outlook: Stable

LR2 – In general, the market remains down between 12% and 22%. Outlook: Negative

Handy – Slow pick-up is possible subject to the easing of lockdowns and demand for refined products on each side of the Atlantic. LR and MR tanker rates, however, are now below those of Handy tankers, meaning that charterers will likely shift to larger vessel sizes, wherever possible. Therefore, we should expect a further drop in Handy rates. Outlook: Negative

Dirty Panamax – Rates softened everywhere, among fears of a new COVID wave due to the delta variant. Outlook: Stable

Dry Cargo

Capesize – Relatively slow uptake in rate growth, with spot demand weakened slightly in western regions due to summer holidays approaching. Outlook: Stable

Panamax – stable demand does not lead to expect a growth in rates going forward. Tendency to slightly weaken counterbalanced by the hold availability shortage. Outlook: Stable

Supramax – rates climbing steadily over the course of 2021 and stabilised in May with no real surge expected. Outlook: Stable

Handysize – rates remained pretty much stable without much movement from the previous weeks.. Outlook: Stable

Container

Container rates continue with their strong rally on all fronts, although the curve seems to be flattening a little bit. Demand looks strong and will continue to be as western economies get out of lockdowns and people shop around for finished goods, using up the savings gathered during the pandemic.

On the raw materials side, however, and especially in chemical commodities, the high freight rates (now looking upwards of $10000 per TEU on the route China – Europe) now impact prices of goods to the extent that it is equivalent or cheaper to source from European suppliers.

We expect to see a continual decrease in smaller-batches shipments westbound from Asia to Europe, hopefully accompanied by a subsequent easing of the TEU rates towards the end of the year.

Outlook: Positive

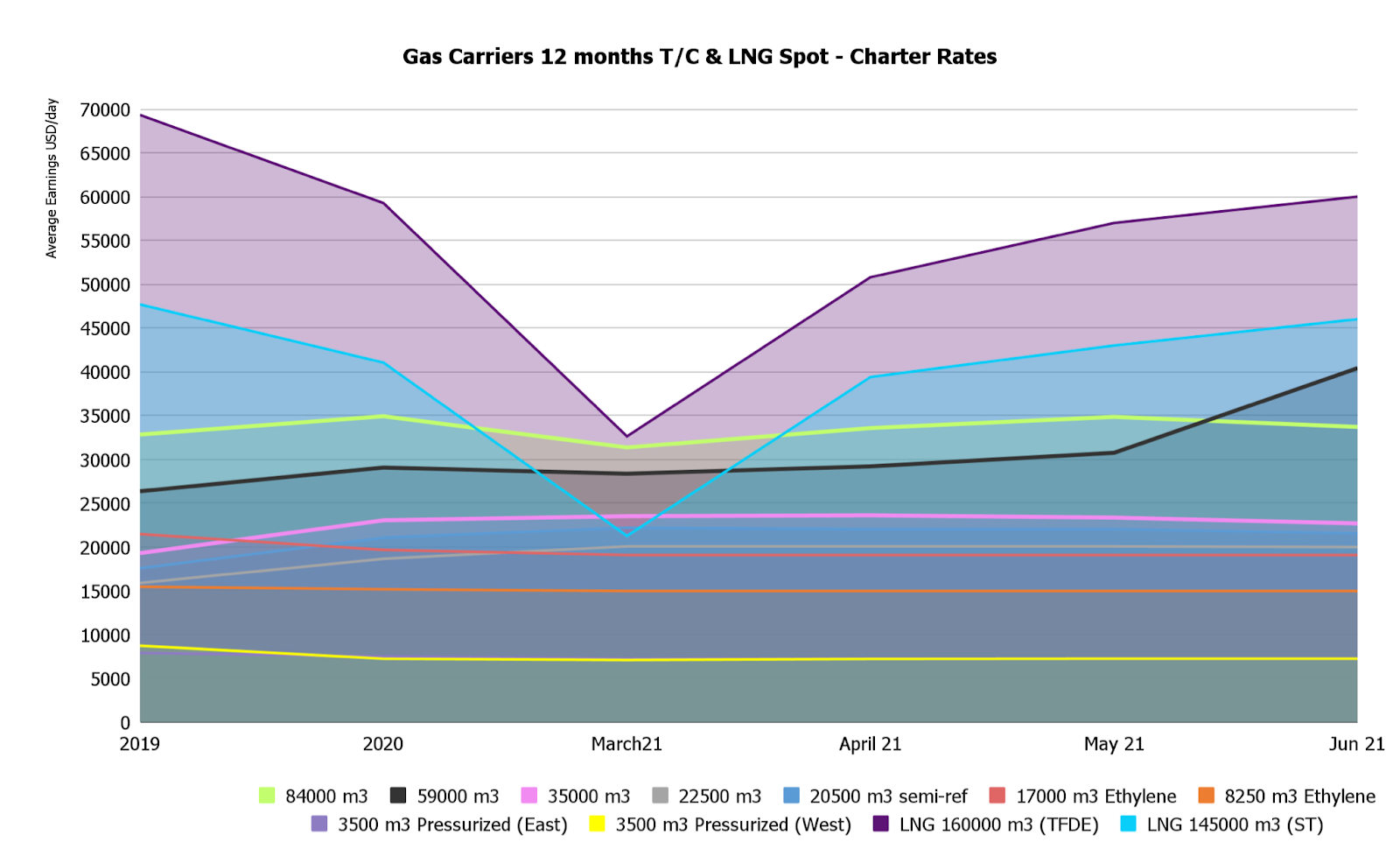

Gas

Rates for Large Gas Carriers slumped up to 39% for large gas carriers. Cargo cancellations were the primary causes, resulting in oversupply of carrying capacity in all main routes. Pressurized and semi-pressurized vessel rates remained unchanged.

As plenty of tonnage is currently tied-up in dock for ballast water treatment systems installation, we are to expect a further softening of the rates next month, as the ships come back into the market.

Outlook: Negative

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK.

Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.

Howdy! This post could not be written any better! Looking through this article reminds

me of my previous roommate! He constantly kept talking about this.

I will send this article to him. Fairly certain he’ll have a very good read.

Many thanks for sharing!